Social Security is a cornerstone of financial security for millions of Americans. It is a program that has been providing financial assistance to retirees, disabled individuals, and survivors for decades. However, over the years, it has faced scrutiny and criticism, with some individuals labeling it as a Ponzi scheme. This term, often associated with fraudulent investment scams, raises concerns about the sustainability and future of the Social Security system. In this article, we will delve into the intricacies of Social Security, examining its structure, purpose, and addressing the question: is social security a ponzi scheme?

For many people, understanding the complexity of the Social Security program can be daunting. With its roots dating back to the 1930s, the program was designed to provide a safety net for Americans who have reached retirement age or are unable to work due to disability. Despite its noble intentions, misconceptions and myths have clouded public perception, leading to debates about its legitimacy and effectiveness. It is important to analyze these claims critically and assess whether they hold any truth.

To better understand the issue and answer the question of whether Social Security is a Ponzi scheme, we need to explore its fundamental principles and compare them with the characteristics of a Ponzi scheme. This article will provide a comprehensive analysis of Social Security, addressing common misconceptions, analyzing its funding mechanisms, and exploring its impact on society. By doing so, we aim to provide clarity on the topic and offer a well-rounded perspective on the future of Social Security.

Table of Contents

- History of Social Security

- The Structure of Social Security

- Understanding Ponzi Schemes

- Comparing Social Security to Ponzi Schemes

- The Funding Mechanism of Social Security

- Social Security and Economic Stability

- Common Misconceptions about Social Security

- The Impact of Demographics on Social Security

- Social Security Reforms and Proposals

- The Role of Social Security in Retirement Planning

- Social Security's Effect on Poverty Reduction

- International Perspectives on Social Security

- The Future of Social Security

- Frequently Asked Questions

- Conclusion

History of Social Security

The Social Security Act was signed into law by President Franklin D. Roosevelt on August 14, 1935. This landmark legislation was part of the New Deal, a series of programs and reforms aimed at revitalizing the American economy during the Great Depression. The primary objective of the Social Security Act was to provide financial support to retired workers, ensuring they had a steady income in their later years.

As the program evolved, it expanded to include benefits for disabled individuals and survivors, further solidifying its role as a critical component of the social safety net. Over the years, Social Security has undergone numerous amendments and changes, reflecting the shifting economic and demographic landscape of the United States.

The program's funding mechanism, primarily through payroll taxes, has been a subject of debate and scrutiny. Despite its challenges, Social Security remains a vital source of income for millions of Americans, with nearly 65 million people receiving benefits as of 2021.

The Structure of Social Security

Social Security is a federal program that operates on a pay-as-you-go basis. This means that current workers' payroll taxes are used to fund the benefits of current retirees. The program is funded primarily through the Federal Insurance Contributions Act (FICA) tax, which is deducted from workers' paychecks. Employers also contribute an equal amount, ensuring a steady stream of revenue to support the program.

The Social Security Administration (SSA) is responsible for administering the program and ensuring that eligible individuals receive their benefits. The SSA calculates benefit amounts based on an individual's earnings history, taking into account the number of years worked and the age at which they begin receiving benefits.

One of the key features of Social Security is its progressive benefit formula, which aims to provide a higher replacement rate for lower-income workers. This ensures that individuals with lower lifetime earnings receive a relatively larger portion of their pre-retirement income, helping to reduce poverty among the elderly.

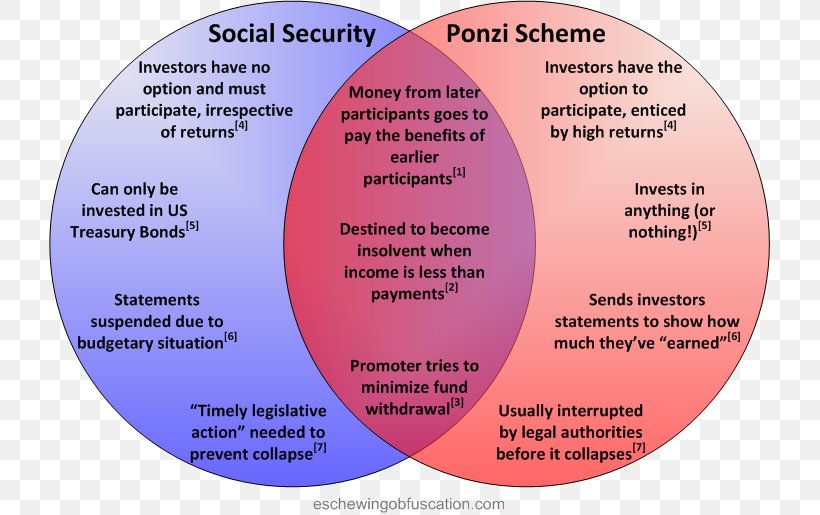

Understanding Ponzi Schemes

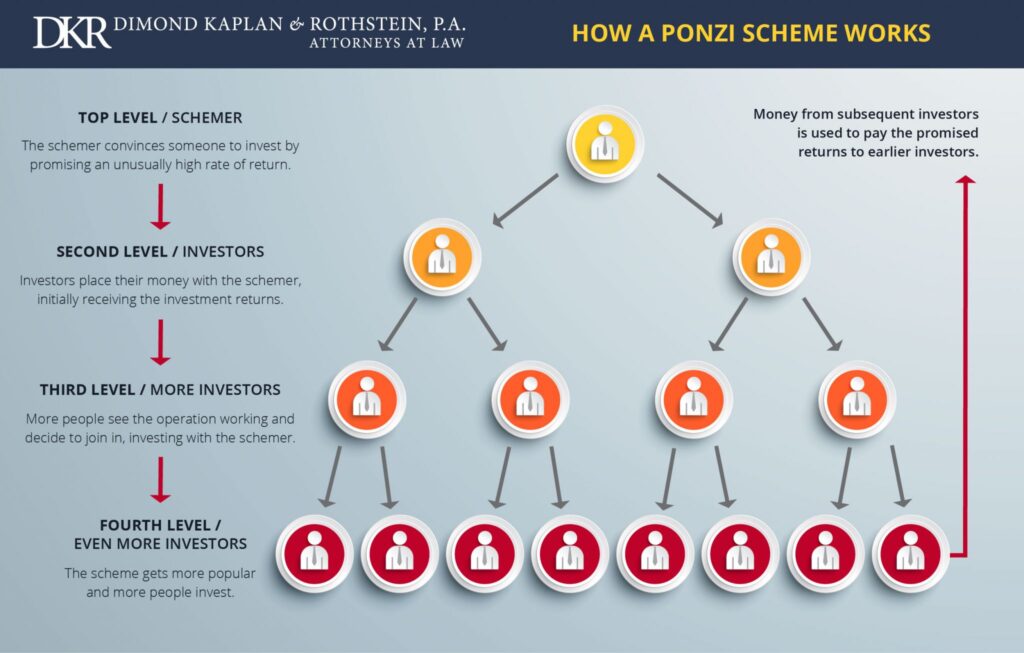

A Ponzi scheme is a type of investment scam that promises high returns with little risk to investors. These schemes rely on attracting new investors to pay returns to earlier investors, rather than generating profits through legitimate business activities. As a result, Ponzi schemes are inherently unsustainable and eventually collapse when they can no longer recruit enough new investors to pay returns.

The term "Ponzi scheme" is named after Charles Ponzi, an infamous swindler who operated a fraudulent investment scheme in the early 20th century. Ponzi promised investors exorbitant returns on their investments by claiming to profit from international postal reply coupons. In reality, he used funds from new investors to pay returns to earlier investors, creating the illusion of a successful investment.

Key characteristics of a Ponzi scheme include the reliance on new investors to pay returns, the lack of legitimate business operations, and the eventual collapse when the scheme can no longer attract new investors.

Comparing Social Security to Ponzi Schemes

While some critics argue that Social Security resembles a Ponzi scheme, there are significant differences between the two. Unlike Ponzi schemes, Social Security is a legitimate government program with a defined purpose and structure. It is not designed to generate profits or provide high returns but rather to provide a safety net for retirees, disabled individuals, and survivors.

One of the key differences is that Social Security is transparent and operates under the oversight of the federal government. The program's funding mechanism, through payroll taxes, is well-documented and regulated, ensuring accountability and stability. Additionally, Social Security is not dependent on recruiting new participants to pay benefits, as it is funded through a combination of payroll taxes, interest on trust fund assets, and income from taxation of benefits.

While Social Security faces financial challenges due to demographic shifts and increasing life expectancy, it is not a fraudulent scheme designed to deceive participants. Instead, it is a vital social program that requires ongoing reform and adaptation to ensure its sustainability for future generations.

The Funding Mechanism of Social Security

Social Security is primarily funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). Workers and their employers each contribute 6.2% of earnings, up to a certain income limit, to fund the program. Self-employed individuals pay the full 12.4% themselves, reflecting both the employee and employer portions.

In addition to payroll taxes, Social Security receives income from interest on the trust fund assets and taxation of benefits. The Social Security Trust Fund is invested in U.S. Treasury securities, which earn interest and provide a source of revenue to support the program.

Despite its current funding challenges, Social Security is projected to be able to pay full benefits until 2034, after which it will still be able to pay approximately 76% of benefits if no changes are made. This underscores the importance of addressing the program's long-term financial health to ensure its continued viability.

Social Security and Economic Stability

Social Security plays a crucial role in promoting economic stability by providing a reliable source of income for retirees, disabled individuals, and survivors. By offering financial support to those who may otherwise struggle to make ends meet, the program helps to reduce poverty and improve the overall quality of life for millions of Americans.

The program also serves as an economic stabilizer, as beneficiaries tend to spend their benefits on essential goods and services, contributing to local economies and supporting businesses. This spending helps to create jobs and stimulate economic growth, particularly in communities with a high concentration of retirees.

Furthermore, Social Security provides a safety net during economic downturns, offering a consistent source of income for beneficiaries even when other sources of income may be disrupted. This stability is particularly important during times of economic uncertainty, such as recessions or financial crises.

Common Misconceptions about Social Security

There are several common misconceptions about Social Security that can lead to confusion and misinformation. One of the most prevalent myths is that Social Security is a Ponzi scheme. As we've discussed, while the program faces challenges, it is fundamentally different from a Ponzi scheme in terms of purpose, structure, and funding.

Another misconception is that Social Security is going bankrupt. While the program does face financial challenges, it is not on the brink of bankruptcy. With appropriate reforms and adjustments, Social Security can continue to provide benefits for future generations.

Some people also believe that Social Security benefits are guaranteed and will never change. In reality, benefits are subject to change due to various factors, such as cost-of-living adjustments, changes in the law, and demographic shifts.

Finally, there is a misconception that Social Security only benefits retirees. In fact, the program provides benefits to a wide range of individuals, including disabled workers, survivors of deceased workers, and certain family members of beneficiaries.

The Impact of Demographics on Social Security

Demographic shifts have a significant impact on the sustainability of Social Security. As the population ages and life expectancy increases, the ratio of workers to beneficiaries decreases, putting pressure on the program's funding.

The aging population is primarily driven by the baby boomer generation reaching retirement age, resulting in a larger number of beneficiaries compared to the number of working-age individuals contributing to the program. This demographic shift is a key factor in the program's projected financial shortfall.

To address these challenges, policymakers may consider a range of options, such as increasing the payroll tax rate, raising the retirement age, or modifying benefits to ensure the program's long-term viability.

Social Security Reforms and Proposals

Over the years, various proposals have been put forward to reform Social Security and address its financial challenges. These proposals aim to ensure the program's sustainability while maintaining its role as a vital social safety net.

Some proposals focus on increasing revenue, such as raising the payroll tax rate or eliminating the income cap on taxable earnings. Others suggest reducing benefits, such as raising the retirement age or adjusting the benefit formula to provide lower benefits for higher-income individuals.

Policymakers have also considered more comprehensive reforms, such as creating individual retirement accounts or implementing a means-tested benefit structure. Each proposal has its own set of advantages and challenges, requiring careful consideration and analysis to determine the best path forward.

The Role of Social Security in Retirement Planning

Social Security is a critical component of retirement planning for many Americans, providing a steady source of income that can help cover essential expenses in retirement. While it is not intended to be the sole source of retirement income, Social Security serves as a foundation upon which individuals can build their retirement savings.

For many retirees, Social Security benefits represent a significant portion of their income, particularly for those with limited savings or other sources of retirement income. As such, understanding how Social Security benefits are calculated and when to claim them is an important aspect of retirement planning.

Individuals can maximize their Social Security benefits by considering factors such as their full retirement age, the impact of early or delayed claiming, and the potential benefits for spouses and survivors.

Social Security's Effect on Poverty Reduction

Social Security has made a significant impact on reducing poverty among the elderly and vulnerable populations. By providing a reliable source of income, the program helps to lift millions of Americans out of poverty and improve their quality of life.

The progressive benefit formula ensures that lower-income individuals receive a larger portion of their pre-retirement income, helping to reduce income inequality and support those in greatest need. For many beneficiaries, Social Security is the primary or sole source of income, underscoring its importance in reducing poverty.

Research has shown that without Social Security benefits, the poverty rate among older adults would be significantly higher, highlighting the program's critical role in promoting economic security and stability.

International Perspectives on Social Security

Social Security programs exist in various forms around the world, each with its own unique structure and funding mechanisms. While the specifics may differ, the underlying goal of providing financial support to retirees and vulnerable populations is a common thread.

Countries with aging populations face similar challenges in ensuring the sustainability of their social security programs. Many have implemented reforms to address demographic shifts and financial pressures, such as raising the retirement age, adjusting benefit formulas, or increasing contributions.

Examining international perspectives on social security can provide valuable insights and lessons for policymakers as they consider potential reforms and solutions for the future of the program in the United States.

The Future of Social Security

The future of Social Security is a topic of ongoing debate and discussion, with concerns about its financial sustainability and ability to meet the needs of future generations. While the program faces significant challenges, it remains a vital component of the social safety net and an essential source of income for millions of Americans.

Policymakers must balance the need for reforms with the program's core mission of providing financial security and support. By addressing the program's financial challenges and considering a range of policy options, it is possible to ensure the continued viability of Social Security for future generations.

Ultimately, the future of Social Security will depend on the willingness of policymakers and the public to engage in meaningful discussions and make informed decisions that prioritize the program's long-term sustainability and success.

Frequently Asked Questions

1. What is a Ponzi scheme, and how does it differ from Social Security?

A Ponzi scheme is a fraudulent investment scam that promises high returns with little risk. It relies on new investors to pay returns to earlier investors, making it inherently unsustainable. Social Security, on the other hand, is a legitimate government program designed to provide financial support to retirees, disabled individuals, and survivors. It operates transparently under federal oversight and is funded through payroll taxes, not the recruitment of new participants.

2. Is Social Security going bankrupt?

No, Social Security is not going bankrupt. While the program faces financial challenges due to demographic shifts and increasing life expectancy, it is projected to pay full benefits until 2034. After that, it can still pay approximately 76% of benefits if no changes are made. Policymakers have various options to address the program's long-term financial health and ensure its continued viability.

3. How is Social Security funded?

Social Security is primarily funded through payroll taxes collected under the Federal Insurance Contributions Act (FICA). Workers and their employers each contribute 6.2% of earnings, up to a certain income limit. The program also receives income from interest on the trust fund assets and taxation of benefits.

4. What role does Social Security play in reducing poverty?

Social Security plays a significant role in reducing poverty among the elderly and vulnerable populations by providing a reliable source of income. The program's progressive benefit formula ensures that lower-income individuals receive a larger portion of their pre-retirement income, helping to alleviate poverty and promote economic security.

5. Can Social Security benefits change over time?

Yes, Social Security benefits can change due to various factors, such as cost-of-living adjustments, changes in the law, and demographic shifts. While benefits are not guaranteed to remain the same, the program aims to provide a consistent source of income for beneficiaries.

6. What are some proposed reforms for Social Security?

Various proposals have been put forward to reform Social Security and address its financial challenges. These include increasing the payroll tax rate, raising the retirement age, modifying the benefit formula, and creating individual retirement accounts. Each proposal has its own set of advantages and challenges, requiring careful consideration and analysis to determine the best path forward.

Conclusion

In conclusion, Social Security is a vital program that provides financial support to millions of Americans. While it faces challenges and criticisms, it is fundamentally different from a Ponzi scheme in terms of purpose, structure, and funding. By understanding the program's intricacies and addressing its financial challenges, we can ensure the continued viability of Social Security for future generations.

Policymakers, the public, and stakeholders must engage in meaningful discussions and make informed decisions to prioritize the program's long-term sustainability and success. With appropriate reforms and adjustments, Social Security can continue to play a critical role in promoting economic security and stability for all Americans.

For more information on Social Security and related topics, visit the official Social Security Administration website: www.ssa.gov.

You Might Also Like

Strategies For Amparex Funding Success: Maximize Your Investment PotentialExclusive Insights: The Allure Of Trump Coin Silver

Jimmy Stewart Net Worth: The Financial Legacy Of An Iconic Hollywood Star

Insights Into Kadenwood Group: A Leader In The CBD Industry

Understanding The Quantity: How Much Weed Is In A Dub?

Article Recommendations

- Georgias Rule Cast Meet The Stars

- Expecting A Baby Ashantis Pregnancy Journey

- Stunning Pixie Cuts Wavy Hair Inspiration Ideas