In the realm of real estate financing, a mortgage note is an indispensable document, often serving as the linchpin between lenders and borrowers. For anyone stepping into the world of property investments or home buying, understanding the nuances of a mortgage note sample can provide crucial insights into the obligations and rights entailed in a mortgage transaction. As a legal document, the mortgage note outlines the terms of the loan agreement, including payment schedules, interest rates, and penalties for default, thereby ensuring that both parties are on the same page regarding the financial contract.

Mortgage notes are not only central to loan agreements but also serve as a potential investment vehicle for individuals and institutions. By purchasing mortgage notes, investors can earn a steady income stream from the interest paid by the borrower. Hence, a well-drafted mortgage note sample can be a valuable asset, offering security to lenders while providing flexibility to borrowers. Understanding how a mortgage note is structured and what it comprises can enable stakeholders to make informed decisions, mitigate risks, and optimize their investment strategies.

In this comprehensive guide, we will delve into the intricacies of a mortgage note sample, exploring its components, variations, and the significance it holds in the financial landscape. Through clear explanations and practical examples, this article aims to demystify the complexities of mortgage notes, empowering readers with the knowledge needed to navigate the often-confusing world of real estate finance effectively. Whether you are a seasoned investor, a first-time homebuyer, or someone keen on understanding mortgage dynamics, this guide is tailored to equip you with the essential information and insights you need.

Table of Contents

- Understanding a Mortgage Note

- Key Components of a Mortgage Note

- Types of Mortgage Notes

- Creating a Mortgage Note Sample: Steps and Considerations

- Legal Significance of a Mortgage Note

- Investing in Mortgage Notes: Opportunities and Risks

- Mortgage Note vs. Deed of Trust: Understanding the Difference

- Common Mistakes in Drafting Mortgage Notes

- The Role of Mortgage Notes in Foreclosure Processes

- Tips for Borrowers and Lenders Regarding Mortgage Notes

- Sample Mortgage Note: A Detailed Analysis

- The Future of Mortgage Notes in Real Estate Financing

- Frequently Asked Questions

- Conclusion

Understanding a Mortgage Note

A mortgage note, often referred to as a promissory note, is a legal instrument that represents the borrower's promise to repay a loan under specified terms. It is a critical component of the mortgage agreement, serving as evidence of the debt and detailing the repayment schedule, interest rate, and other pertinent loan terms. The mortgage note is signed by the borrower(s) and held by the lender until the loan is paid in full.

The significance of the mortgage note extends beyond its role as a legal document. It is a binding contract that safeguards the interests of both parties involved in the transaction. For borrowers, the mortgage note outlines their obligations and provides a clear understanding of the financial commitment they are undertaking. For lenders, it offers a measure of security, ensuring they have a legal claim to the borrower's property in the event of default.

Understanding the intricacies of a mortgage note is essential for anyone involved in real estate transactions. The document not only delineates the terms of the loan but also establishes the legal framework for enforcement of those terms. By familiarizing themselves with the structure and content of a mortgage note, borrowers and lenders can ensure that their rights and responsibilities are clearly defined and protected.

Key Components of a Mortgage Note

A well-drafted mortgage note comprises several essential components that collectively define the terms and conditions of the loan agreement. These components include:

- Principal Amount: The initial sum of money borrowed by the borrower, exclusive of any interest or fees.

- Interest Rate: The percentage charged by the lender on the principal amount, usually expressed on an annual basis. The interest rate can be fixed or variable, depending on the terms agreed upon.

- Repayment Schedule: The timeline for repayment of the loan, including the frequency of payments (e.g., monthly, quarterly) and the duration of the loan term.

- Payment Amount: The specific amount to be paid by the borrower at each scheduled payment interval. This includes both principal and interest components.

- Late Payment Penalties: Any additional fees or charges imposed on the borrower for failing to make timely payments.

- Prepayment Terms: Provisions relating to the borrower's ability to pay off the loan before the scheduled maturity date, along with any associated penalties or fees.

- Default Clauses: Conditions under which the lender can declare the loan in default, typically as a result of missed payments or other breaches of the agreement.

- Acceleration Clause: A provision allowing the lender to demand full repayment of the loan in the event of default or other specified conditions.

Each of these components plays a vital role in defining the financial relationship between the borrower and lender, and together they form the foundation of a comprehensive mortgage note sample.

Types of Mortgage Notes

Mortgage notes come in various forms, each tailored to meet the specific needs of borrowers and lenders. Understanding the different types of mortgage notes can help stakeholders choose the option that best aligns with their financial objectives and risk tolerance. Common types of mortgage notes include:

- Fixed-Rate Mortgage Note: This type of note features a constant interest rate throughout the loan term, providing borrowers with predictable monthly payments. Fixed-rate mortgage notes are popular among borrowers who prefer stability and want to avoid fluctuations in interest rates.

- Adjustable-Rate Mortgage (ARM) Note: Unlike fixed-rate notes, ARM notes have an interest rate that can change periodically based on prevailing market conditions. These notes typically offer lower initial interest rates, making them attractive to borrowers who anticipate future increases in income or falling interest rates.

- Interest-Only Mortgage Note: This note allows borrowers to pay only the interest portion of the loan for a specified period, after which they must begin repaying the principal as well. Interest-only notes can be beneficial for borrowers expecting significant future cash flows or those seeking to minimize initial payments.

- Balloon Mortgage Note: Balloon notes require borrowers to make relatively small payments for a set period, followed by a large "balloon" payment to pay off the remaining balance. These notes are suitable for borrowers who plan to refinance or sell the property before the balloon payment becomes due.

- Convertible Mortgage Note: This note provides borrowers with the option to convert from an adjustable-rate to a fixed-rate mortgage, offering flexibility to adapt to changing financial circumstances.

Each type of mortgage note carries its own set of advantages and potential drawbacks. Careful consideration of these factors is essential when selecting the most appropriate note for a given situation.

Creating a Mortgage Note Sample: Steps and Considerations

Drafting a mortgage note sample involves several key steps and considerations to ensure that the document accurately reflects the terms of the loan agreement and protects the interests of both parties. The following steps outline the process of creating a mortgage note sample:

- Define the Terms of the Loan: Begin by clearly defining the principal amount, interest rate, repayment schedule, and any other terms agreed upon by the borrower and lender. These terms should be mutually acceptable and reflect the financial capabilities and objectives of both parties.

- Consult Legal Experts: Engage legal professionals to review the draft mortgage note and ensure that it complies with applicable laws and regulations. Legal expertise is crucial to identifying potential issues and mitigating the risk of future disputes.

- Include Essential Clauses: Incorporate key clauses such as late payment penalties, prepayment terms, default clauses, and acceleration clauses. These clauses are vital for establishing clear expectations and safeguarding the interests of both parties.

- Ensure Clarity and Precision: Use clear and precise language to articulate the terms of the loan. Ambiguities or vague wording can lead to misunderstandings and disputes, which can be costly and time-consuming to resolve.

- Obtain Signatures: Once the mortgage note is finalized, obtain signatures from both the borrower and lender to formalize the agreement. Signatures are essential for establishing the legal binding nature of the document.

Creating a mortgage note sample is a meticulous process that requires careful attention to detail and a thorough understanding of the legal and financial implications involved. By following these steps and seeking professional guidance, stakeholders can ensure that their mortgage note is comprehensive, accurate, and legally sound.

Legal Significance of a Mortgage Note

The legal significance of a mortgage note cannot be overstated, as it serves as the foundation of the borrower-lender relationship in a real estate transaction. This document is legally binding and outlines the borrower's commitment to repay the loan under the specified terms. In the event of a dispute or default, the mortgage note serves as evidence of the agreement and provides a basis for legal enforcement.

The mortgage note is distinct from the mortgage itself, which is the security instrument that grants the lender a lien on the property. While the mortgage secures the lender's interest in the property, the mortgage note establishes the borrower's obligation to repay the loan. Together, these documents form the legal framework for the mortgage transaction.

In the context of foreclosure, the mortgage note plays a critical role in determining the lender's rights and remedies. If the borrower defaults on the loan, the lender can enforce the terms of the mortgage note through legal action, potentially resulting in the sale of the property to recover the outstanding debt. Understanding the legal significance of a mortgage note is essential for both borrowers and lenders to protect their interests and navigate the complexities of real estate finance effectively.

Investing in Mortgage Notes: Opportunities and Risks

Investing in mortgage notes offers unique opportunities for individuals and institutions seeking to diversify their portfolios and generate steady income streams. By purchasing mortgage notes, investors effectively step into the shoes of the lender, receiving interest payments from borrowers and potentially benefiting from the appreciation of the underlying property.

One of the primary advantages of investing in mortgage notes is the potential for attractive returns. Mortgage notes often offer higher yields compared to traditional fixed-income investments, making them an appealing option for yield-seeking investors. Additionally, mortgage notes can provide a measure of diversification, as they are typically less correlated with other asset classes such as stocks and bonds.

However, investing in mortgage notes also carries inherent risks that investors must carefully consider. Key risks include:

- Credit Risk: The risk that the borrower will default on the loan, resulting in a loss of principal and interest.

- Interest Rate Risk: The risk that changes in interest rates will negatively impact the value of the mortgage note.

- Liquidity Risk: The risk that the investor may not be able to sell the mortgage note quickly or at a favorable price.

- Market Risk: The risk that changes in the real estate market will affect the value of the underlying property and, consequently, the mortgage note.

To mitigate these risks, investors should conduct thorough due diligence, including assessing the creditworthiness of the borrower, the value of the underlying property, and the terms of the mortgage note. By carefully evaluating these factors and diversifying their mortgage note investments, investors can enhance their potential for success and minimize their exposure to risk.

Mortgage Note vs. Deed of Trust: Understanding the Difference

While the terms "mortgage note" and "deed of trust" are often used interchangeably, they represent distinct legal instruments with different implications for borrowers and lenders. Understanding the differences between these documents is crucial for navigating real estate transactions effectively.

A mortgage note is a promissory note that outlines the borrower's obligation to repay the loan under specified terms. It serves as evidence of the debt and details the repayment schedule, interest rate, and other pertinent terms. The mortgage note is signed by the borrower(s) and held by the lender until the loan is paid in full.

In contrast, a deed of trust is a security instrument that grants the lender a lien on the property to secure the loan. In a deed of trust arrangement, a third party known as a trustee holds the title to the property until the loan is repaid. If the borrower defaults, the trustee has the authority to sell the property through a foreclosure process to satisfy the debt.

The key differences between a mortgage note and a deed of trust include:

- Parties Involved: A mortgage note involves two parties—the borrower and the lender—while a deed of trust involves three parties—the borrower, lender, and trustee.

- Foreclosure Process: The foreclosure process for a deed of trust is typically non-judicial, meaning it does not require court involvement, while a mortgage foreclosure is usually judicial, requiring legal proceedings.

- Title Holding: In a deed of trust arrangement, the trustee holds the title to the property, whereas in a mortgage arrangement, the borrower retains the title.

Understanding these distinctions is essential for borrowers and lenders to make informed decisions and choose the legal instrument that best aligns with their needs and objectives.

Common Mistakes in Drafting Mortgage Notes

Drafting a mortgage note is a complex process that requires careful attention to detail and a thorough understanding of the legal and financial implications involved. Common mistakes in drafting mortgage notes can lead to misunderstandings, disputes, and costly legal battles. To avoid these pitfalls, stakeholders should be aware of the following common mistakes:

- Ambiguous Language: Using vague or ambiguous language in a mortgage note can lead to misunderstandings and disputes. It is essential to use clear and precise language to articulate the terms of the loan and avoid potential ambiguities.

- Omitting Essential Clauses: Failing to include key clauses such as late payment penalties, prepayment terms, default clauses, and acceleration clauses can leave the parties vulnerable to disputes and legal challenges.

- Inadequate Legal Review: Failing to consult legal experts to review the draft mortgage note can result in non-compliance with applicable laws and regulations, increasing the risk of legal issues.

- Inaccurate Financial Terms: Inaccuracies in the financial terms of the loan, such as the interest rate or repayment schedule, can lead to disputes and financial losses. It is crucial to ensure that all financial terms are accurate and align with the agreed-upon terms.

- Failure to Obtain Signatures: Failing to obtain signatures from both the borrower and lender can render the mortgage note unenforceable, undermining its legal validity.

By being aware of these common mistakes and taking proactive steps to address them, stakeholders can ensure that their mortgage note is comprehensive, accurate, and legally sound.

The Role of Mortgage Notes in Foreclosure Processes

Mortgage notes play a critical role in foreclosure processes, serving as the foundation of the lender's legal claim to the borrower's property. In the event of a default, the lender can enforce the terms of the mortgage note through legal action, potentially resulting in the sale of the property to recover the outstanding debt.

The foreclosure process typically begins when the borrower fails to make timely payments as specified in the mortgage note. The lender may issue a notice of default, informing the borrower of the delinquency and providing an opportunity to cure the default. If the borrower fails to cure the default, the lender can proceed with foreclosure proceedings.

The specific foreclosure process varies depending on the type of security instrument used (i.e., mortgage or deed of trust) and the jurisdiction. In a judicial foreclosure, the lender must file a lawsuit in court to obtain a judgment allowing the sale of the property. In a non-judicial foreclosure, the lender can foreclose without court involvement, typically through a trustee sale.

Throughout the foreclosure process, the mortgage note serves as evidence of the borrower's obligation to repay the loan and the lender's right to enforce the terms of the agreement. Understanding the role of mortgage notes in foreclosure processes is essential for both borrowers and lenders to navigate the complexities of real estate finance effectively.

Tips for Borrowers and Lenders Regarding Mortgage Notes

For borrowers and lenders, understanding the intricacies of mortgage notes is essential for navigating real estate transactions effectively and protecting their interests. The following tips offer practical guidance for both parties:

Tips for Borrowers:

- Read the Mortgage Note Carefully: Take the time to read and understand all the terms and conditions outlined in the mortgage note. Seek clarification on any ambiguous or unclear language.

- Understand Your Obligations: Familiarize yourself with your repayment obligations, including the payment schedule, interest rate, and any penalties for late or missed payments.

- Keep Communication Open: Maintain open communication with your lender, especially if you encounter financial difficulties that may impact your ability to make timely payments.

- Consult Legal Experts: Engage legal professionals to review the mortgage note and ensure that it complies with applicable laws and regulations.

Tips for Lenders:

- Ensure Clarity and Precision: Use clear and precise language to articulate the terms of the loan and avoid potential ambiguities.

- Include Essential Clauses: Incorporate key clauses such as late payment penalties, prepayment terms, default clauses, and acceleration clauses.

- Conduct Thorough Due Diligence: Assess the creditworthiness of the borrower and the value of the underlying property to mitigate risk.

- Seek Legal Expertise: Consult legal experts to review the draft mortgage note and ensure compliance with applicable laws and regulations.

By following these tips, borrowers and lenders can ensure that their mortgage note is comprehensive, accurate, and legally sound, ultimately protecting their interests and facilitating a successful real estate transaction.

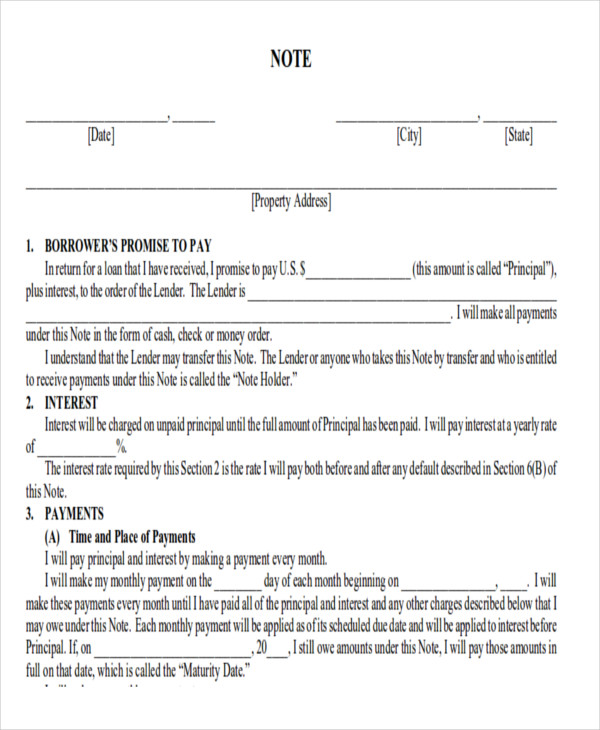

Sample Mortgage Note: A Detailed Analysis

Analyzing a sample mortgage note can provide valuable insights into the structure and content of this critical document. A typical mortgage note sample includes various sections, each serving a specific purpose in defining the terms of the loan agreement. The following analysis highlights key components of a mortgage note sample:

Header and Identification:

The header section identifies the document as a mortgage note and includes pertinent information such as the date of issuance, the names and addresses of the borrower and lender, and the property address.

Principal and Interest:

This section specifies the principal amount of the loan, the interest rate, and the method of calculating interest. It also outlines the total amount to be repaid, including both principal and interest components.

Repayment Terms:

The repayment terms section details the payment schedule, including the frequency of payments (e.g., monthly, quarterly) and the duration of the loan term. This section also specifies the amount of each payment and any grace periods for late payments.

Default and Acceleration Clauses:

This section outlines the conditions under which the lender can declare the loan in default, as well as the consequences of default. It also includes an acceleration clause, allowing the lender to demand full repayment of the loan in the event of default or other specified conditions.

Prepayment and Late Payment Penalties:

This section specifies any penalties or fees associated with prepaying the loan or making late payments. It also outlines the borrower's rights and obligations regarding prepayment.

By analyzing a sample mortgage note, stakeholders can gain a deeper understanding of the document's structure and content, ultimately enhancing their ability to navigate real estate transactions effectively.

The Future of Mortgage Notes in Real Estate Financing

The future of mortgage notes in real estate financing is likely to be shaped by various trends and developments, including technological advancements, regulatory changes, and evolving market dynamics. As the real estate landscape continues to evolve, mortgage notes will remain a critical component of property transactions, offering both challenges and opportunities for stakeholders.

One significant trend shaping the future of mortgage notes is the increasing adoption of digital technologies and automation. With advancements in blockchain technology and smart contracts, the process of drafting, executing, and managing mortgage notes is becoming more streamlined and efficient. These technologies offer the potential to enhance transparency, reduce fraud, and improve the overall efficiency of real estate transactions.

Regulatory changes are also likely to impact the future of mortgage notes. As governments and regulatory bodies continue to implement new policies and guidelines to promote transparency and consumer protection, stakeholders must stay informed and adapt to changing regulatory requirements to ensure compliance and mitigate risk.

Additionally, evolving market dynamics, such as changing interest rates, property values, and borrower preferences, will continue to influence the structure and content of mortgage notes. Stakeholders must remain agile and responsive to these changes to optimize their investment strategies and navigate the complexities of real estate finance effectively.

Overall, the future of mortgage notes in real estate financing is poised to be dynamic and multifaceted, offering both challenges and opportunities for borrowers, lenders, and investors alike.

Frequently Asked Questions

1. What is a mortgage note sample?

A mortgage note sample is a template or example of a mortgage note document that outlines the terms and conditions of a loan agreement between a borrower and a lender. It serves as a reference for drafting a comprehensive and legally sound mortgage note.

2. How does a mortgage note differ from a deed of trust?

A mortgage note is a promissory note that outlines the borrower's obligation to repay the loan, while a deed of trust is a security instrument that grants the lender a lien on the property. A deed of trust involves a third party known as a trustee, who holds the title to the property until the loan is repaid.

3. What are the key components of a mortgage note?

The key components of a mortgage note include the principal amount, interest rate, repayment schedule, payment amount, late payment penalties, prepayment terms, default clauses, and acceleration clauses.

4. What are the risks of investing in mortgage notes?

The risks of investing in mortgage notes include credit risk, interest rate risk, liquidity risk, and market risk. Investors should conduct thorough due diligence and diversify their investments to mitigate these risks.

5. How can I create a mortgage note sample?

To create a mortgage note sample, define the terms of the loan, consult legal experts, include essential clauses, ensure clarity and precision, and obtain signatures from both the borrower and lender to formalize the agreement.

6. What role does a mortgage note play in foreclosure processes?

A mortgage note serves as evidence of the borrower's obligation to repay the loan and the lender's right to enforce the terms of the agreement. In foreclosure processes, the mortgage note is used to establish the lender's legal claim to the borrower's property.

Conclusion

Mortgage notes are a fundamental component of real estate financing, serving as the legal foundation for loan agreements between borrowers and lenders. Understanding the intricacies of a mortgage note sample is essential for navigating real estate transactions effectively and protecting the interests of all parties involved. By familiarizing themselves with the structure and content of mortgage notes, stakeholders can make informed decisions, mitigate risks, and optimize their investment strategies. As the real estate landscape continues to evolve, mortgage notes will remain a critical instrument, offering both challenges and opportunities for borrowers, lenders, and investors alike. Through comprehensive analysis and careful consideration, stakeholders can harness the potential of mortgage notes to achieve their financial objectives and navigate the complexities of real estate finance with confidence.

You Might Also Like

Hawaii's Lucrative Opportunity: A Deep Dive Into Mineral Rights For SaleJohn Stankey Net Worth: Insights Into The Business Mogul's Financial Success

Jetty Deposit: Your Ultimate Guide To Understanding Its Value

Daddy Dave Net Worth: A Look Into The Life And Success Of A Racing Icon

Proof Coins: An In-Depth Guide To Their Unique Craft And Value

Article Recommendations

- Expecting A Baby Ashantis Pregnancy Journey

- Ron Palillo Net Worth 2024 A Deep Dive

- Kat Timpfs Husband Meet Husbands Name