Securing a home can be a daunting task, especially in the dynamic real estate market of Connecticut. However, the FHA loan CT presents an accessible pathway for many aspiring homeowners. This government-backed loan program is specifically designed to cater to individuals who may find it challenging to meet the stringent requirements of conventional loans. With lower down payment options and flexible credit qualifications, FHA loans provide a viable solution for individuals and families looking to own a home in the beautiful state of Connecticut.

FHA loans, or Federal Housing Administration loans, are a type of mortgage insured by the federal government. This insurance protects lenders against losses if a borrower defaults on the loan. The FHA loan program was established as part of the National Housing Act of 1934, aiming to increase homeownership in America by making housing loans more accessible to a broader range of people, including first-time homebuyers and those with less-than-perfect credit scores. In Connecticut, FHA loans are a popular choice due to their affordability and flexibility, making it easier for residents to achieve their dream of homeownership.

Connecticut, known for its scenic landscapes and vibrant communities, offers an array of real estate opportunities, from charming suburban homes to bustling city apartments. However, the state also presents some unique challenges in the housing market, such as high property prices and varying regional economic conditions. This is where the FHA loan CT becomes particularly beneficial. By providing financial support through lower down payments and competitive interest rates, FHA loans empower potential homeowners to navigate these challenges effectively and secure a home that suits their needs and budget.

Table of Contents

- Understanding FHA Loans

- Benefits of FHA Loan CT

- Eligibility Requirements

- Application Process

- FHA Loan Limits in Connecticut

- FHA vs. Conventional Loans

- Common Misconceptions

- Managing Your FHA Loan

- Refinancing Options

- Impact on Credit Score

- Role of Lenders

- Importance of Inspections

- Protecting Your Investment

- Future of FHA Loans

- FAQs

Understanding FHA Loans

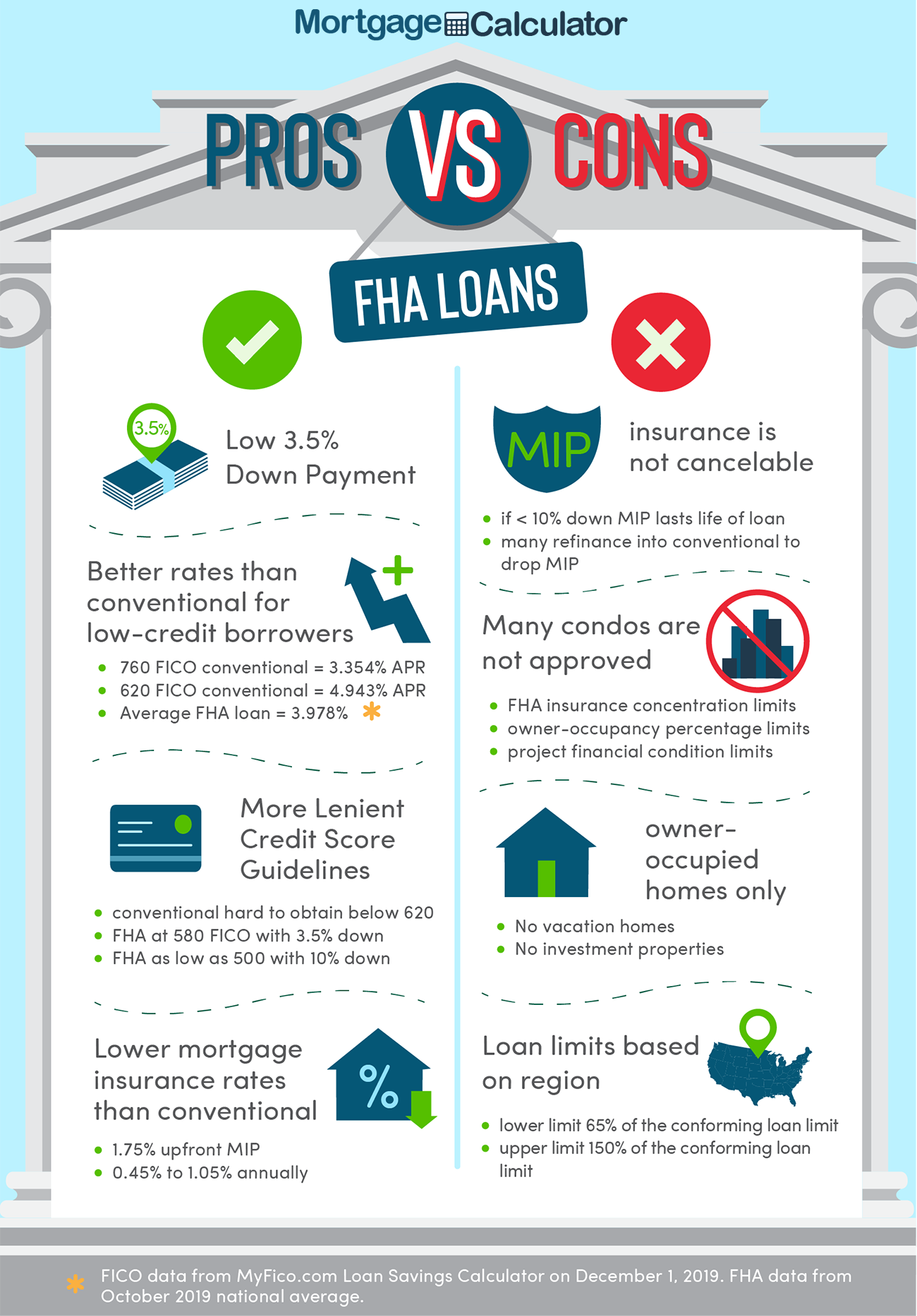

FHA loans are government-insured mortgages designed to help more Americans afford homeownership. The Federal Housing Administration, a part of the U.S. Department of Housing and Urban Development (HUD), insures these loans. This insurance reduces the risk for lenders, making them more willing to offer loans to a broader range of applicants, including those with lower credit scores or smaller down payments. FHA loans are particularly beneficial for first-time homebuyers, those with limited savings, and individuals with a less-than-perfect credit history.

One of the defining features of FHA loans is the lower down payment requirement. While traditional loans might require a down payment of 20% or more, FHA loans allow for as little as 3.5% down. This significantly lowers the barrier to entry for potential homeowners who might struggle to save for a larger down payment. Additionally, FHA loans offer more lenient credit score requirements. While conventional loans often require a credit score of 620 or higher, FHA loans may be available to borrowers with scores as low as 580, or even 500 in some cases, with a higher down payment.

Another aspect of FHA loans is the mortgage insurance premium (MIP). Since FHA loans are insured, borrowers are required to pay MIP, which protects the lender in case of default. There are two types of MIP: an upfront premium paid at closing and an annual premium that is spread out over the life of the loan. The upfront premium is typically 1.75% of the loan amount, while the annual premium varies based on the loan term and amount. Despite the added cost of MIP, many borrowers find the benefits of FHA loans outweigh the expense, especially when compared to the challenges of qualifying for a conventional loan.

Benefits of FHA Loan CT

FHA loans in Connecticut offer several advantages that make them an attractive option for potential homeowners. One of the primary benefits is the ability to purchase a home with a lower down payment. This is particularly advantageous in Connecticut, where property prices can be high, making it difficult for many to save up for a traditional down payment. With FHA loans, buyers can purchase a home with as little as 3.5% down, significantly reducing the initial financial burden.

Another benefit of FHA loans is the flexibility in credit score requirements. Connecticut residents with lower credit scores may find it challenging to qualify for conventional loans, which often require a score of 620 or higher. FHA loans, on the other hand, may be available to borrowers with scores as low as 580, or even 500 with a larger down payment. This opens up homeownership opportunities to a broader range of people, including those who are recovering from past financial difficulties.

FHA loans also offer competitive interest rates, which can be particularly appealing in a state like Connecticut, where the cost of living is relatively high. These rates are often lower than those of conventional loans, making monthly payments more affordable. Additionally, FHA loans are assumable, meaning that if you sell your home, the buyer can take over your mortgage, potentially making your property more attractive to prospective buyers.

Eligibility Requirements

To qualify for an FHA loan in Connecticut, borrowers must meet several eligibility requirements. First and foremost, the borrower must have a valid Social Security number, be a lawful resident of the United States, and be of legal age to sign a mortgage in Connecticut. Additionally, the property being purchased must serve as the borrower's primary residence.

Credit score requirements for FHA loans are more lenient than those for conventional loans. A minimum credit score of 580 is typically required to qualify for the FHA's 3.5% down payment program. However, borrowers with a credit score between 500 and 579 may still qualify for an FHA loan, provided they can make a down payment of at least 10%. It's important to note that while these are the FHA's minimum requirements, individual lenders may have their own credit score requirements.

Debt-to-income ratio (DTI) is another critical factor in determining FHA loan eligibility. The FHA typically requires a DTI ratio of no more than 43%. This means that your monthly debt payments, including your mortgage, must not exceed 43% of your gross monthly income. In some cases, borrowers with a DTI ratio as high as 50% may still qualify if they have other compensating factors, such as a high credit score or substantial savings.

Application Process

The application process for an FHA loan in Connecticut involves several steps, starting with choosing a reputable FHA-approved lender. It's essential to research and compare different lenders to find one that offers the best terms and conditions for your needs. Once you've selected a lender, you'll need to complete a mortgage application, providing detailed information about your financial situation, including your income, assets, debts, and employment history.

After submitting your application, the lender will perform a thorough review of your financial information, including a credit check. This step is crucial, as it helps the lender determine your eligibility for an FHA loan and the terms they can offer you. If your application is approved, the lender will provide you with a pre-approval letter, which you can use to show sellers that you're a serious buyer with the financial backing to purchase their property.

Next, you'll need to find a property that meets the FHA's minimum property standards. These standards are in place to ensure that the home is safe, sound, and secure for the borrower. Once you've found a property, you'll need to have it appraised by an FHA-approved appraiser. The appraiser will assess the property's value and condition to ensure it meets the FHA's requirements. If the appraisal is satisfactory, you can proceed with the closing process, during which you'll finalize your loan and become a homeowner.

FHA Loan Limits in Connecticut

FHA loan limits in Connecticut vary by county and are determined based on the median home prices in each area. These limits are set by the Federal Housing Administration and are subject to change annually. The limits are designed to ensure that FHA loans are available to a wide range of borrowers, while also reflecting the local real estate market conditions.

In general, FHA loan limits in Connecticut tend to be higher in areas with more expensive housing markets, such as Fairfield County, which includes cities like Stamford and Greenwich. Conversely, in areas with lower median home prices, such as Windham County, the limits may be lower. It's essential for prospective homebuyers to be aware of the specific FHA loan limits in their desired area, as this will impact the maximum loan amount they can qualify for.

For the most accurate and up-to-date information on FHA loan limits in Connecticut, it's recommended to visit the U.S. Department of Housing and Urban Development (HUD) website or consult with a local FHA-approved lender. Understanding these limits is crucial for planning your home purchase and ensuring that you select a property that falls within your budget and qualifying criteria.

FHA vs. Conventional Loans

When deciding between an FHA loan and a conventional loan, it's essential to understand the key differences and how they may impact your homebuying experience. FHA loans are government-insured, which allows for lower down payments and more lenient credit requirements. This makes them an attractive option for first-time homebuyers or those with less-than-perfect credit. However, FHA loans require mortgage insurance premiums, which can add to the overall cost of the loan.

Conventional loans, on the other hand, are not government-insured and typically require a higher credit score and a larger down payment, often around 20%. These loans may be a better option for borrowers with strong credit profiles and sufficient savings for a substantial down payment. Additionally, conventional loans usually do not require private mortgage insurance (PMI) if the down payment is 20% or more, which can lead to lower monthly payments compared to FHA loans.

Ultimately, the decision between an FHA and a conventional loan will depend on your financial situation, credit history, and homeownership goals. It's crucial to carefully weigh the pros and cons of each option and consult with a mortgage professional to determine the best fit for your needs.

Common Misconceptions

There are several misconceptions surrounding FHA loans that may deter potential borrowers from considering them as a viable option. One common misconception is that FHA loans are only available to first-time homebuyers. While they are popular among this group, FHA loans are available to any eligible borrower, regardless of whether they have previously owned a home.

Another misconception is that FHA loans are only for low-income individuals. While they are designed to make homeownership more accessible, there are no income limits for FHA loans. Borrowers of all income levels can qualify, provided they meet the other eligibility requirements. Additionally, some people believe that FHA loans are more challenging to obtain than conventional loans, but in reality, the more lenient credit and down payment requirements often make them more accessible to a broader range of borrowers.

By understanding the facts about FHA loans and dispelling these misconceptions, potential homebuyers can make more informed decisions about their financing options and ultimately achieve their homeownership goals.

Managing Your FHA Loan

Once you've secured an FHA loan and purchased your home, it's essential to manage your loan effectively to ensure long-term financial stability. This includes making timely monthly mortgage payments, maintaining a good credit score, and budgeting for any additional expenses, such as property taxes, insurance, and maintenance costs.

One key aspect of managing your FHA loan is understanding your mortgage insurance premium (MIP) obligations. As a borrower, you'll be required to pay both an upfront MIP at closing and an annual MIP as part of your monthly mortgage payments. It's crucial to factor these costs into your budget and plan accordingly to avoid any financial strain.

Additionally, it's essential to stay in communication with your lender and address any potential issues, such as financial hardships, as soon as they arise. Many lenders offer assistance programs for borrowers experiencing temporary financial difficulties, which can help you maintain your home and avoid foreclosure.

Refinancing Options

As a homeowner with an FHA loan, you may have the opportunity to refinance your mortgage to take advantage of lower interest rates or more favorable loan terms. One popular refinancing option is the FHA Streamline Refinance program, which allows borrowers to refinance their existing FHA loan with minimal documentation and no appraisal requirement. This can be an attractive option for homeowners looking to reduce their monthly payments or shorten the term of their loan.

Another option is to refinance into a conventional loan, which may be beneficial if you've built up enough equity in your home to eliminate the need for mortgage insurance. This can lead to significant savings over the life of the loan, particularly if you can secure a lower interest rate. It's essential to carefully consider your refinancing options and consult with a mortgage professional to determine the best course of action for your financial situation and goals.

Impact on Credit Score

Obtaining an FHA loan can have both positive and negative impacts on your credit score. On the positive side, making timely mortgage payments can help improve your credit score over time, demonstrating your ability to manage debt responsibly. Additionally, as you pay down your loan balance and build equity in your home, your credit utilization ratio may improve, further boosting your credit score.

However, it's essential to be aware of potential negative impacts as well. Applying for an FHA loan will result in a hard inquiry on your credit report, which can temporarily lower your score. Additionally, if you struggle to make your mortgage payments or miss payments altogether, your credit score could suffer. To mitigate these risks, it's crucial to budget carefully, make timely payments, and communicate with your lender if you encounter any financial difficulties.

Role of Lenders

Lenders play a crucial role in the FHA loan process, as they are responsible for evaluating your eligibility, processing your application, and providing the necessary financing to purchase your home. When choosing a lender, it's essential to research and compare different options to find one that offers competitive rates and terms, as well as excellent customer service.

Once you've selected a lender, they will guide you through the application process, helping you gather the necessary documentation and ensuring that your application is complete and accurate. The lender will also coordinate with the appraiser and underwriter to assess the property's value and condition and determine your eligibility for the loan.

Throughout the life of your loan, your lender will continue to play a vital role, handling your mortgage payments, managing your escrow account, and providing support and assistance if you encounter any issues or have questions about your loan. Building a strong relationship with your lender can help ensure a smooth and successful homeownership experience.

Importance of Inspections

When purchasing a home with an FHA loan, it's essential to conduct thorough inspections to ensure that the property meets the FHA's minimum property standards and is a sound investment. While the FHA requires an appraisal to assess the property's value and condition, this is not a substitute for a comprehensive home inspection conducted by a licensed professional.

A home inspection can identify potential issues or defects that may not be apparent during a casual walkthrough, such as structural problems, plumbing or electrical issues, or signs of water damage. By uncovering these issues upfront, you can address them with the seller before closing or factor them into your decision to purchase the property.

Conducting a thorough inspection can help protect your investment and ensure that you're making an informed decision about your home purchase. It's essential to work with a reputable home inspector and carefully review their findings to make the best choice for your needs and budget.

Protecting Your Investment

Once you've purchased a home with an FHA loan, it's crucial to take steps to protect your investment and ensure its long-term value. This includes maintaining your property, making necessary repairs, and staying informed about local market trends and property values.

Regular maintenance and upkeep can help prevent costly repairs and extend the life of your home's major systems, such as the roof, HVAC, and plumbing. Additionally, staying informed about your local real estate market can help you make strategic decisions about when to refinance, sell, or make improvements to your property.

By taking a proactive approach to managing and maintaining your home, you can protect your investment and ensure that it remains a valuable asset for years to come.

Future of FHA Loans

The future of FHA loans in Connecticut and across the nation will likely be shaped by various factors, including changes in housing market conditions, government policy, and economic trends. As the real estate market continues to evolve, FHA loans may adapt to meet the needs of a diverse range of borrowers and address emerging challenges in the housing sector.

One potential area of growth for FHA loans is the increased focus on sustainable and energy-efficient housing. As more homebuyers prioritize environmentally friendly homes, the FHA may expand its offerings to include loans specifically designed for energy-efficient improvements or green building practices.

Additionally, as housing prices continue to rise in many areas, FHA loan limits may be adjusted to better reflect local market conditions and ensure that the program remains accessible to a broad range of borrowers. By staying informed about these trends and changes, potential homebuyers can better understand their options and make informed decisions about their financing needs.

FAQs

- What is the minimum credit score required for an FHA loan in Connecticut? The minimum credit score required for an FHA loan is typically 580 for a 3.5% down payment. However, borrowers with lower scores may qualify with a larger down payment.

- Can I use an FHA loan to buy a second home or investment property? No, FHA loans are intended for primary residences only. They cannot be used to purchase second homes or investment properties.

- Are there income limits for FHA loans? No, there are no income limits for FHA loans. They are available to borrowers of all income levels, provided they meet the other eligibility requirements.

- How long do I have to pay mortgage insurance on an FHA loan? Mortgage insurance is required for the life of the loan if your down payment is less than 10%. If your down payment is 10% or more, you may be able to cancel the insurance after 11 years.

- Can I refinance my FHA loan into a conventional loan? Yes, you can refinance your FHA loan into a conventional loan if you meet the credit and equity requirements. This can eliminate the need for mortgage insurance and potentially lower your monthly payments.

- Are FHA loans assumable? Yes, FHA loans are assumable, meaning that a buyer can take over your mortgage if you sell your home. This can make your property more attractive to potential buyers.

You Might Also Like

Strategic Branding In Real Estate Investing: A Guide To Names And SuccessMartin Flyer: The Pinnacle Of Fine Jewelry Craftsmanship

Your Guide To David Brickman: A Trailblazer In Finance

Coq Inu Price Prediction: Future Prospects And Insights

Upcoming Ex-Dividend Date For IEP: A Detailed Guide

Article Recommendations

- Ron Palillo Net Worth 2024 A Deep Dive

- Black Lab Pit Mix Lifespan Average Factors Affecting It

- Stunning Pixie Cuts Wavy Hair Inspiration Ideas